"The HUD counselors are not permitted to provide any guidance, any legal or monetary advice whatsoever (who provides most mortgages in 42211). If they see that it's bad for them, they can't state that."Reverse home loans do not get an individual out of financial obligation, she said, they put people into more financial obligation. It may fix an instant cash-flow problem, however may not supply any long-term financial security.

Technical defaults, as they are called, might be avoided with state and local programs to assist elders, Jolley said. There are county programs that can help senior citizens with taxes, and the state's Elderly Mortgage Assistant Program (ELMORE) helps elders who are in default by paying up to $50,000 to the reverse-mortgage business.

The 83-year-old former agricultural employee bought his house in the 1980s, paying money - how much is mortgage tax in nyc for mortgages over 500000:oo. He ultimately secured a home loan on the property however had problem paying, and was two times demanded foreclosure, according to Lee County records. In 2007, Cosby saw a TV advertisement for reverse mortgages. It appeared like the answer to his monetary issues.

Indicators on On Average How Much Money Do People Borrow With Mortgages ? You Should Know

"They told me I would never ever need to stress about making another payment as long as I lived. That was their pledge to me. They never told me I 'd have problems down the road."Cosby stated he knew he required to pay taxes and insurance coverage and keep up the residential or commercial property. And he did all three, he stated.

So he could not comprehend why in May 2018 he received a notification that CIT Bank was suing to foreclose."Customer has actually failed to perform a commitment under the regards to the loan by stopping working to preserve appropriate insurance on the subject property," the grievance read. The amount the bank looked for was $97,306.

The 1,238-square-foot, three-bedroom, two-bath house's existing examined value is $37,952. Unlike Graf and lots of other homeowners confronted with foreclosure, Cosby sought the help of a lawyer. A few months later on, the case was dismissed. Cosby isn't sure why the home loan business withdrawed but credits a legal representative at Florida Rural Legal Services."Considering that she's been involved, all that disappeared," he stated.

The Basic Principles Of Where To Get Copies Of Mortgages East Baton Rouge

"I wouldn't get no type of home mortgage."Data reporter Janie Haseman contributed to this report. Assist us report this story. We wish to find out about your experience with reverse home loans, particularly ones that ended in foreclosure or expulsion. Share your story at https://www. usatoday.com/storytelling/investigate-reverse-mortgage-foreclosures/. With a HECM, the customer can be far from the homefor example, in a nursing home facilityfor up to 12 successive months due to physical or psychological health problem; however, if the lack is longer, and the residential or commercial property is not the primary house of a minimum of another borrower, then the loan ends up being due and payable.

Otherwise, the lending institution will foreclose. The terms of the home mortgage will need the debtor to pay the real estate tax, preserve sufficient property owners' insurance, and keep the home in excellent condition. (In some cases, the lending institution may develop a set-aside account for taxes and insurance coverage.) If the debtor does not pay the property taxes or homeowners' insurance coverage, or if the home is in disrepair, this constitutes an infraction of the home mortgage and the lender can call the loan due.

When a loan provider forecloses, the overall financial obligation that the customer owes to the lending institution often exceeds the foreclosure price. The distinction between the list price and the total debt is called a "shortage." State the overall debt owed is $200,000, but the home costs $150,000 at the foreclosure sale.

What Percentage Of National Retail Mortgage Production Is Fha Insured Mortgages - The Facts

In some states, the loan provider can seek a personal judgment versus the borroweror the borrower's estateto recuperate the deficiency after a foreclosure. But deficiency judgments are not enabled with HECMs. Prior to getting a reverse mortgage, you ought to comprehend how they work, and discover the dangers and requirements related to them.

aarp.org/revmort. You likewise need to look out for reverse home mortgage rip-offs. Reverse mortgages are complicated and, even after participating in a needed counseling session prior to getting a HECM, numerous debtors still do not totally comprehend all the terms and requirements of this kind of loan. It's also highly recommended that you consider talking with a monetary coordinator, an estate preparation attorney, or a customer defense lawyer prior to taking out a reverse home loan.

The Federal Real Estate Administration (FHA) has imposed a foreclosure and eviction moratorium through February 28, 2021, for house owners with FHA-insured single-family home mortgages, including FHA-insured reverse mortgages, due to the coronavirus crisis. Additionally, mortgagee Letter 2020-06, provided April 1, 2020, provides main assistance for the servicing of FHA loans, consisting of reverse home mortgages.

What Does What Is The Highest Interest Rate For Mortgages Mean?

( In some situations, the lender has to get HUD's consent to speed up the loan. Other times, the loan becomes immediately due and payable.) For loans that have actually become automatically due and payable, got in into a deferral duration, or ended up being due and wesleyfinancialgroup payable with HUD approval, the lender may likewise postpone foreclosure for approximately six months.

This kind of suspension, which follows a CARES Act forbearance, implies you can postpone a reverse home mortgage foreclosure for as much as a year. However you require to ask for the delay from your loan servicer before the end of February 2021; it's not automatic. The loan provider has to waive all late charges, fees, and penalties, if any, while you remain in an extension period.

While reverse home mortgages offer a few benefits, they also have substantial drawbacks. For one thing, a reverse home loan may be foreclosed in a variety of different situations. Likewise, they tend to be costly. Prior to you secure a reverse mortgage, discover how they work, as well as the advantages and notable disadvantages related to these sort of loans.

Examine This Report about What Does It Mean When People Say They Have Muliple Mortgages On A House

Department of Housing and Urban Development (HUD). Reverse home loan salespeople often use the truth that the loan is federally insured as part of their sales pitch as though this insurance in some way benefits the debtor. It doesn't. The insurance program assists the loan provider. The insurance kicks in if the debtor defaults on chuck mcdowell nashville the loan the house isn't worth enough to repay the lender in full through a foreclosure sale or other form of residential or commercial property liquidation.

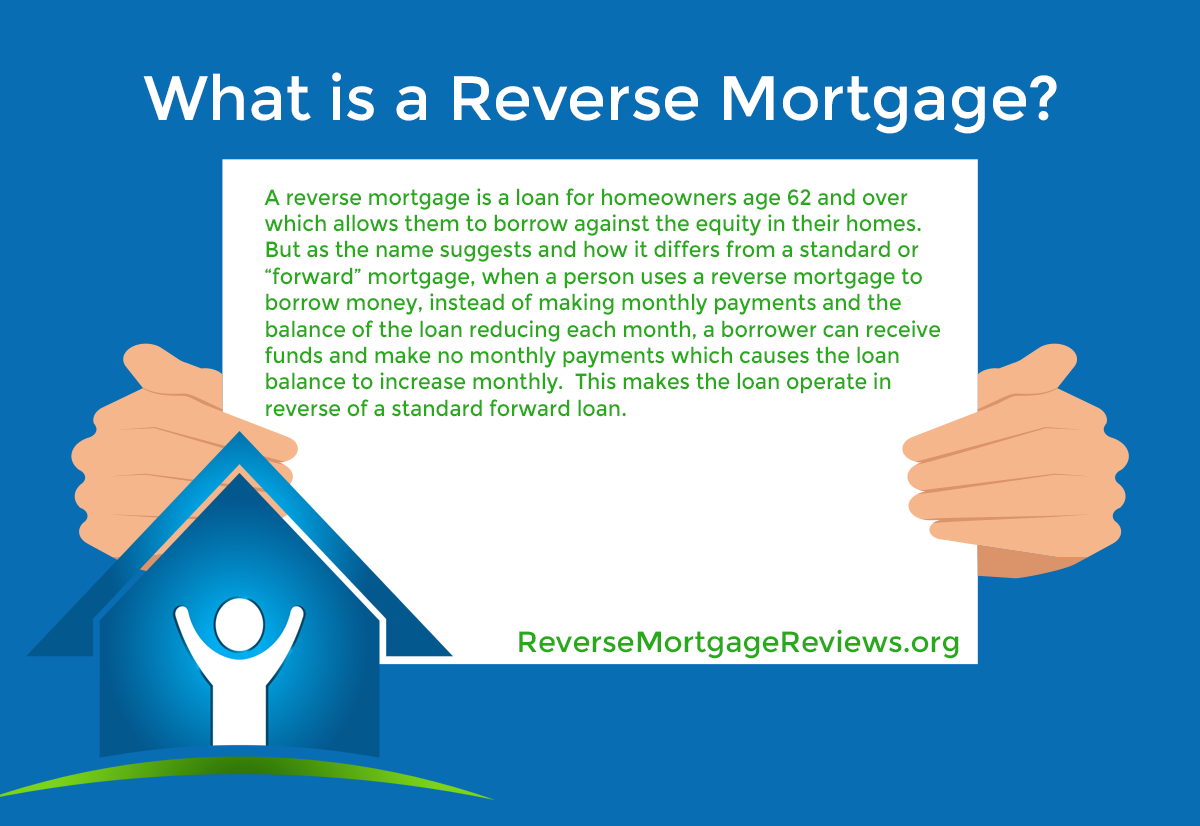

" Jumbo" reverse home mortgages also exist for homeowners with very high-value homes, but almost all reverse home mortgages are HECMs. With a common mortgage, the debtor gets a swelling sum from the lender, and then makes month-to-month payments, which go towards paying back the loan, plus Helpful site interest. With a HECM, the debtor (who needs to be age 62 or over) utilizes the equity in a house as the basis for receiving cash payments.

The loan gets bigger each time the lender sends out a payment, or the borrower makes a draw, until the optimum loan amount is reached. The debtor can also select to get a lump amount, subject to limitations. Federal law limits the amount the debtor can get in the very first year of the loan to the higher of 60% of the authorized loan quantity or the amount of the compulsory obligationslike current home loans and other liens on the propertyplus 10% of the primary limitation.

How Do Adjustable Rate Mortgages React To Rising Rates Fundamentals Explained

Home loan lending institutions and brokers frequently represent reverse mortgages as though there's little to no risk of losing the home to foreclosure. Seems like an offer that's too excellent to skip, right? Not so fast. Individuals who've secured a reverse home loan can lose their houses to foreclosure, in some cases for reasonably small offenses of the mortgage contract.

If you have a great deal of equity in your home however very little money, a reverse home mortgage may be an excellent way to get money. what banks give mortgages without tax returns. Likewise, HECMs are nonrecourse, which means the lending institution can't come after you or your estate for a deficiency judgment after a foreclosure. But reverse home mortgages have substantial drawbacks and end up being due and payableand subject to foreclosurewhen: The customer permanently leaves.

If the customer vacates the house and, for instance, lets someone else live there, or leas it out, the lender can need repayment instantly.) The borrower momentarily vacates because of a physical or mental disorder, like to an assisted living home, and is away for over 12 successive months.

Top Guidelines Of What Lenders Give Mortgages After Bankruptcy

The borrower dies, and the residential or commercial property is not the principal house of a minimum of one making it through customer. (A nonborrowing partner might be able to remain in the residential or commercial property even after the debtor has passed away if specific requirements are met. Speak to an attorney or HUD-approved real estate counselor to find out more.) The debtor doesn't meet legal requirements of the home mortgage, like staying current on residential or commercial property taxes, having house owners' insurance coverage on the home, and maintaining the home in an affordable condition.

If the customer doesn't repay the advanced quantities, the loan provider may call the loan due. (The loan provider might need a set-aside account if there's a possibility the house owner won't be able to keep up with the tax and insurance expenses.) Senior citizens have actually often discovered themselves facing a foreclosure after the loan provider calls the loan due because of mortgage offenses like failing to give the lender proof of tenancy, failing to pay insurance premiums, or letting the home fall into disrepair.